3 Sep 2022

The RDHonest-vStata package implements estimates and

confidence intervals (CIs) from Armstrong and Kolesár (2018) and Armstrong and

Kolesár (2020) for regression discontinuity (RD) in Stata. This

vignette describes some of the functionality. Section 2 discusses sharp RD. Section 3 discusses fuzzy RD. Section 4 discusses some extensions that are not

currently implemented in the RDHonest-vStata package along

with references to other software packages that implement them when

applicable.

To begin, we’ll illustrate using elections data from Lee (2008).

. clear all

. macro drop _all

. webuse set "https://raw.githubusercontent.com/tbarmstr/RDHonest-vStata/master/data"

(prefix now "https://raw.githubusercontent.com/tbarmstr/RDHonest-vStata/master/data")

. webuse lee08

(Lee, D. S. (2008))The running variable margin is margin of victory of the

Democratic candidate in the previous election in percentage points. The

outcome variable voteshare is the Democratic candidate’s

share of the vote in the next election, in percentage points. The cutoff

is 0.

The rdhonest command implements honest CIs based on

local linear estimates. For illustration, let’s start with the uniform

kernel.

. * uniform kernel, defaults for other options:

. * Armstrong and Kolesár (2020) rule of thumb for M + MSE optimal bandwidth

. rdhonest voteshare margin, kernel("uni")

Using Armstrong and Kolesar (2020) rule of thumb for smoothness constant M

Honest inference: SHARP Regression Discontinuity

──────────────────────────────────────────────────────────────────────────────

Estimate Maximum Bias Std. Error [ 95% Conf. intervals ]

──────────────────────────────────────────────────────────────────────────────

4.79816988 .891210516 1.57140644 1.2829887 8.31335106

──────────────────────────────────────────────────────────────────────────────

95% One-sided Conf. intervals: (1.32222577 , Inf), (-Inf, 8.27411398)

Bandwidth (optimized): 6.01199567

Number of effective observations: 728

Parameters:

Cutoff: 0

Kernel: uniform

Optimization criterion: MSE

Standard error estimation method: NN

Maximum leverage for estimated parameter: .006421319

Smoothness constant M (rule of thumb): .142810807

──────────────────────────────────────────────────────────────────────────────

Dependent variable: voteshare

Running variable: margin When we use the uniform kernel, the point estimate is simply obtained

by running a linear regression using a “discontinuity sample” of

observations within a certain distance of the cutoff (note that the

cutoff is 0 in this example, which is the default for the

rdhonest command; we can specify a different cutoff using

the option c()). The distance that determines the

discontinuity sample is called the bandwidth. It is given in the output

above, and can be obtained using the postestimation

e(bandwidth):

. display e(bandwidth)

6.0119957So, in this case, we are running a linear regression using observations where the running variable is within 6.0119957 units of the cutoff point 0. We can check that the point estimates match using Stata’s built-in commands:

. scalar bw = e(bandwidth)

. gen treat = (margin>0)

. gen treatxmargin = treat*margin

. reg voteshare treat margin treatxmargin if abs(margin)<=bw, robust

Linear regression Number of obs = 728

F(3, 724) = 53.20

Prob > F = 0.0000

R-squared = 0.1832

Root MSE = 11.495

─────────────┬────────────────────────────────────────────────────────────────

│ Robust

voteshare │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

treat │ 4.79817 1.614018 2.97 0.003 1.629456 7.966884

margin │ .9246502 .3048005 3.03 0.003 .3262519 1.523049

treatxmargin │ -.0081335 .4760755 -0.02 0.986 -.9427869 .9265199

_cons │ 46.99352 1.061989 44.25 0.000 44.90857 49.07847

─────────────┴────────────────────────────────────────────────────────────────Note that, while the point estimates match, the standard errors are

slightly different. This is due to the rdhonest command

defaulting to a nearest-neighbor (NN) standard error, rather than the

usual EHW standard error. The NN standard error can be less conservative

in certain settings, but here the two methods yield similar results.

A more striking difference is the 95% CI computed by the built-in

regression command, which is slightly shorter than the one reported by

rdhonest. The rdhonest command computes a

bias-aware CI that explicitly takes into account the largest

possible bias in a smoothness class determined by a

smoothness constant \(M\). In

particular, rather than assuming the specification in the above

regression holds exactly, we assume that it holds only up to

approximation error:

\[ \text{voteshare}_i = \tau \cdot \text{treat}_i + \beta_1 + \beta_2 \text{margin}_i + \beta_3 \text{treat}_i\cdot \text{margin}_i + \text{rem}(\text{margin}_i) + u_i \]

where \(\text{treat}_i=I(\text{margin}_i>0)\)

and \(\text{rem}(\text{margin}_i)\) is

the remainder term from a first order Taylor approximation of the

conditional expectation function of voteshare given margin by the linear

specification on either side of the cutoff point. We assume that this

remainder term comes from a Taylor approximation where this conditional

expectation function is twice differentiable, with second derivative

bounded by \(M\). The

rdhonest command allows \(M\) to be specified throught the

m() option. If this option is not specified (as in the

example above), it uses a rule-of-thumb from Armstrong and Kolesár (2020)

that calibrates \(M\) based on a global

fourth order polynomial on either side of the cutoff. The maximum bias

and smoothness constant are displayed in the output for

rdhonest. It can be obtained in postestimation with

e(bias) and e(M).

The two-sided CI reported by rdhonest uses the critical

value \(\text{cv}_{\alpha}(t)\),

computed as the \(1-\alpha\) quantile

of the \(|N(0,t)|\) distribution, with

\(t=\frac{\text{max.

bias}}{\text{se}}\):

\[ \text{estimate} \pm \text{cv}_{\alpha}\left(\frac{\text{max. bias}}{\text{se}}\right)\cdot \text{se} \]

By taking into account the maximum possible bias, this critical value

ensures that the coverage of the CI is at least \(1-\alpha\). The level \(\alpha\) is set using the option

alpha() and defaults to \(.05\). We refer to this as a

fixed-length CI, since it depends only on the standard error

and the smoothness constant \(M\). Note

that one could also add and subtract \(\text{max. bias} + z_{1-\alpha/2}\cdot

\text{se}\) to form the CI. Indeed, the one-sided CIs reported by

rdhonest take this form: the lower endpoint of the lower

one-sided CI is \[

\text{estimate} - \text{max. bias} - z_{1-\alpha}\cdot \text{se}

\] where \(z_{1-\alpha}\) is the

\(1-\alpha\) quantile of the \(N(0,1)\) distribution. However, in the

two-sided case, the above construction is less conservative.

The identifying assumption in sharp RD is that the latent conditional

expectation functions for treated and untreated outcomes are smooth. The

smoothness class described above formalizes this in a way that allows

for valid inference and guarantees on estimation error. The CIs reported

by rdhonest are honest in the sense that coverage

is close to the nominal level or better for all functions in this class

once the sample size is large enough. In addition, since these CIs use

finite-sample bounds on bias, the only thing needed for good

finite-sample coverage is accuracy of the normal approximation. In

particular, they are valid with discrete covariates.

Some users may be more familiar with

“pointwise-in-the-underlying-distribution” formulations of smoothness.

These are used, for example, in the optimal bandwidth calculations of

Imbens and Kalyanaraman

(2012). For many practical purposes, the two formulations lead to

similar conclusions and interpretations. For example, the mean squared

error optimal bandwidth (computed by rdhonest and discussed

below) turns out to have the same asymptotic formula as the one used by

Imbens and Kalyanaraman

(2012), with \(M\) in our

setting taking the place of the second derivative (or difference in

second derivatives) in Imbens and Kalyanaraman (2012). Indeed,

one can loosely think of the honest CI formulation used by

rdhonest as a “decision theoretically kosher” version of

pointwise-in-the-underlying distribution smoothness formulations. Key

practical differences are:

The honest CI formulation used by rdhonest can be

used in finite samples, thereby allowing for discrete

covariates.

The honest CI formulation treats \(M\) as a bound on the second derivative, rather than an exact value of the second derivative. This precludes higher order bias correction without further assumptions on higher derivatives. If one makes assumptions on higher order derivatives, this is done in the honest CI framework by formulating a bound \(M_{\text{higher}}\) on this derivative and optimally using this bound to form estimates and CIs.

See Section 4 of Armstrong and Kolesár (2020) for further discussion.

If the bandwidth is unspecified (as in the above example)

rdhonest computes the bandwidth that optimizes a given

criterion for the smoothness class characterized by the bound \(M\) on the second derivative of the

regression function. The criterion can be set using the option

opt_criterion(). Options are MSE for mean

squared error, FLCI for two-sided CI length and

OCI for excess length of a one-sided CI, with

MSE set as the default.

The optimization is done using an initial estimate of the conditional

variance. Because rdhonest reports a robust standard error

and a bias-aware CI based on this standard error, the variance estimate

used to optimize the CI will be different than the one used for the

reported standard error and CI.

The fact that different criteria lead to different point estimates is

potentially irksome: we may want to report a point estimate that

optimizes MSE, while using the FLCI option to

report a CI that is as small as possible. This can be easily done by

rerunning the rdhonest command with both options, but one

may be hesitant to report a CI that is not centered at the reported

point estimate. Fortunately, a result from Armstrong and Kolesár (2020)

shows that, under standard RD asymptotics, MSE and CI length lead to

very similar bandwidths, and that using the MSE optimal bandwidth to

compute a bias-aware CI is still highly efficient. Let’s see how much we

can reduce the length of our CI by choosing the bandwidth to minimize CI

length:

. * same specification as before, but choose the bandwidth to minimize CI length

. rdhonest voteshare margin, kernel("uni") opt_criterion("FLCI")

Using Armstrong and Kolesar (2020) rule of thumb for smoothness constant M

Honest inference: SHARP Regression Discontinuity

──────────────────────────────────────────────────────────────────────────────

Estimate Maximum Bias Std. Error [ 95% Conf. intervals ]

──────────────────────────────────────────────────────────────────────────────

5.14231308 .951187869 1.57124452 1.5754211 8.70920506

──────────────────────────────────────────────────────────────────────────────

95% One-sided Conf. intervals: (1.60665797 , Inf), (-Inf, 8.67796819)

Bandwidth (optimized): 6.18426502

Number of effective observations: 750

Parameters:

Cutoff: 0

Kernel: uniform

Optimization criterion: FLCI

Standard error estimation method: NN

Maximum leverage for estimated parameter: .00612847

Smoothness constant M (rule of thumb): .142810807

──────────────────────────────────────────────────────────────────────────────

Dependent variable: voteshare

Running variable: margin The bandwidth, point estimate, and CI are all very similar to the ones based on the MSE optimal bandwidth above. In this case, the MSE optimal bandwidth actually leads to a slightly shorter CI than the CI optimal bandwidth. This is due to different variance estimates being used to compute the bandwidth and the CI, as described above.

The rdhonest package also includes an option to specify

the bandwidth directly, through the option h(). However,

this may lead to a bandwidth that is far from optimal for the smoothness

constant \(M\) specified through

m(), or through the default rule-of-thumb. Rather than

specifying the bandwidth directly, we recommend specifying the

smoothness constant \(M\) through the

m() option, and letting the rdhonest command

compute the optimal bandwidth. Since the optimal bandwidth depends

directly on \(M\), this is equivalent

to checking sensitivity of results to the bandwidth. We discuss this

below.

An exception to this practice arises if the optimal bandwidth leads

to a very small number of effective observations, which may lead to poor

finite-sample performance of the CI due to failure of the normal

approximation. One may then want to use the option h() to

specify a larger bandwidth.

As shown in Armstrong and Kolesár (2018), it is

impossible to avoid specifying the smoothness constant \(M\), either explicitly or using auxiliary

assumptions, such as the assumptions described in Armstrong and Kolesár (2020)

relating a global polynomial to local smoothness that motivate the

rule-of-thumb used by rdhonest as a default. We therefore

recommend varying \(M\) as a form of

sensitivity analysis. Since we let rdhonest compute the

optimal bandwidth for each value of \(M\), this is equivalent to reporting

specifications with different bandwidths.

Let’s try some other choices of \(M\) in our original specification. We’ll start with the default Armstrong and Kolesár (2020) rule-of-thumb, and then consider more optimistic (smaller) choices of \(M\), and more pessimistic (larger) choices of \(M\).

. qui rdhonest voteshare margin, kernel("uni")

. scalar M_rot = e(M)

. scalar est_rot = e(est)

. scalar HLCi_rot = e(HLCi)

. scalar h_rot = e(bandwidth)

.

. * some other values of M to try

. scalar M01 = .1*M_rot

. scalar M05 = .5*M_rot

. scalar M2 = 2*M_rot

. scalar M10 = 10*M_rot

.

. qui rdhonest voteshare margin, kernel("uni") m(`=M01')

. scalar est01 = e(est)

. scalar HLCi01 = e(HLCi)

. scalar h01 = e(bandwidth)

.

. qui rdhonest voteshare margin, kernel("uni") m(`=M05')

. scalar est05 = e(est)

. scalar HLCi05 = e(HLCi)

. scalar h05 = e(bandwidth)

.

. qui rdhonest voteshare margin, kernel("uni") m(`=M2')

. scalar est2 = e(est)

. scalar HLCi2 = e(HLCi)

. scalar h2 = e(bandwidth)

.

. qui rdhonest voteshare margin, kernel("uni") m(`=M10')

. scalar est10 = e(est)

. scalar HLCi10 = e(HLCi)

. scalar h10 = e(bandwidth)

.

. disp _newline "M | bw | est. | lower CI | upper CI " _newline ///

> round(M01,.0001) " | " round(h01,.0001) " | " round(est01,.0001) " | " round(est01-HLCi01,.0001) " | " round(est01+HLCi01,.0001) _newline ///

> round(M05,.0001) " | " round(h05,.0001) " | " round(est05,.0001) " | " round(est05-HLCi05,.0001) " | " round(est05+HLCi05,.0001) _newline ///

> round(M_rot,.0001) " | " round(h_rot,.0001) " | " round(est_rot,.0001) " | " round(est_rot-HLCi_rot,.0001) " | " round(est_rot+HLCi_rot,.0001) _n

> ewline ///

> round(M2,.0001) " | " round(h2,.0001) " | " round(est2,.0001) " | " round(est2-HLCi2,.0001) " | " round(est2+HLCi2,.0001) _newline ///

> round(M10,.0001) " | " round(h10,.0001) " | " round(est10,.0001) " | " round(est10-HLCi10,.0001) " | " round(est10+HLCi10,.0001)

M | bw | est. | lower CI | upper CI

.0143 | 15.0777 | 7.7854 | 5.5526 | 10.0181

.0714 | 7.9692 | 6.0282 | 3.0281 | 9.0283

.1428 | 6.012 | 4.7982 | 1.283 | 8.3134

.2856 | 4.5821 | 5.2085 | 1.4933 | 8.9236

1.4281 | 2.4064 | 10.7135 | 5.8504 | 15.5766Note that we have used the postestimation e(HLCi) to get

the half-length of the bias-aware CI, which we add and subtract from the

point estimate to get our bias-aware CI.

In this case, the finding of a positive effect size is quite robust: it persists even when we take \(M\) to be 10 times the rule-of-thumb value, which corresponds to a bandwidth of about 2.4.

While we have been using the uniform kernel so far,

rdhonest also includes other kernel options, which can be

specified using the kernel() option. The default is the

triangular kernel:

. rdhonest voteshare margin

Using Armstrong and Kolesar (2020) rule of thumb for smoothness constant M

Honest inference: SHARP Regression Discontinuity

──────────────────────────────────────────────────────────────────────────────

Estimate Maximum Bias Std. Error [ 95% Conf. intervals ]

──────────────────────────────────────────────────────────────────────────────

5.84973224 .88800705 1.36588331 2.69443541 9.00502906

──────────────────────────────────────────────────────────────────────────────

95% One-sided Conf. intervals: (2.71504707 , Inf), (-Inf, 8.98441741)

Bandwidth (optimized): 7.71506984

Number of effective observations: 764.559585

Parameters:

Cutoff: 0

Kernel: triangular

Optimization criterion: MSE

Standard error estimation method: NN

Maximum leverage for estimated parameter: .009560868

Smoothness constant M (rule of thumb): .142810807

──────────────────────────────────────────────────────────────────────────────

Dependent variable: voteshare

Running variable: margin This is numerically equivalent to a weighted least squares regression, with weights decreasing linearly from \(1\) at the cutoff to \(0\) when the running variable is equal to the bandwidth:

. scalar bw = e(bandwidth)

. gen kern_wgt = (1-abs(margin/bw))*((1-abs(margin/bw))>0)

.

. reg voteshare treat margin treatxmargin [weight=kern_wgt], robust

(analytic weights assumed)

(sum of wgt is 462.4894459116331)

Linear regression Number of obs = 936

F(3, 932) = 58.63

Prob > F = 0.0000

R-squared = 0.1573

Root MSE = 11.346

─────────────┬────────────────────────────────────────────────────────────────

│ Robust

voteshare │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

treat │ 5.849732 1.396805 4.19 0.000 3.108485 8.590979

margin │ .6235424 .2295346 2.72 0.007 .1730779 1.074007

treatxmargin │ .1217772 .3545124 0.34 0.731 -.573958 .8175123

_cons │ 46.31878 .9083813 50.99 0.000 44.53607 48.10149

─────────────┴────────────────────────────────────────────────────────────────As before, we obtain the same point estimates, but different CIs due

to rdhonest explicitly taking into account bias.

The triangular kernel is used as a default due to its simplicity and high efficiency (as shown by Armstrong and Kolesár (2020), it is 97.28% efficient relative to the optimal kernel derived by Gao (2018), whereas the uniform kernel is 91.65% efficient). Indeed, here we see that the bias-aware CI based on the triangular kernel is somewhat shorter than the one based on the uniform kernel.

For sharp RD, the rdhonest command gives valid CIs for

discrete as well as continuous running variables. This is because the

worst-case bias calculation holds in finite samples, following Armstrong and Kolesár

(2018). In particular, it does not require asymptotic

approximations that use assumptions on the running variable.

Furthermore, if observations near the cutoff are omitted in a “doughnut

design,” the rdhonest command automatically takes into

account additional bias from extrapolating the regression function to

the cutoff point.

The estimators used by rdhonest are linear

estimators: they can be written as a linear combination of the

outcome \(y_i\) with weights \(w_i\) depending on the entire sample of the

running variable \(x_i\):

\[ \text{estimate} = \sum_{i=1}^n w_i y_i \]

We refer to these as estimation weights. The estimation

weights can be saved as a new variable using the

savewgtest() option:

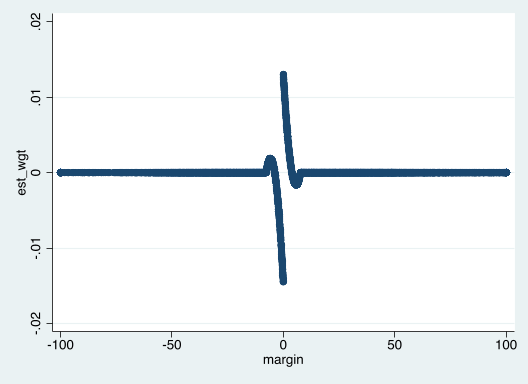

. * triangular kernel

. qui rdhonest voteshare margin, savewgtest(est_wgt)We can then plot the weights \(w_i\) against the running variable \(x_i\):

. scatter est_wgt marginPlots of this form were popularized by Gelman and Imbens (2017). Such plots can be used to assess which values of the running variable are influential in our estimate. In particular, we see that the weights are nonzero only for observations in the discontinuity sample, where the running variable is close to the cutoff point (\(0\) in this case).

The estimation weights also play an important role in the calculation of worst-case bias used to form the bias-aware CI. To give an intuitive description of this, recall that the worst-case bias is calculated using a bound on error from a Taylor approximation at the cutoff. Choosing an estimator with estimation weights \(w_i\) that are zero for \(x_i\) far away from the cutoff (which can be done by choosing a small enough bandwidth) ensures that the approximation error is not too large. We give a more detailed discussion of how the estimation weights are used to calculate the maximum bias in the next section. This section can be skipped by readers not interested in technical details.

As discussed above, rdhonest computes bias-aware CIs

based on the maximum bias under the assumption that the conditional

expectation of the outcome variable given the running variable has

second derivative bounded by the smoothness constant \(M\) on either side of the cutoff. This

section describes the formula for maximum bias. It can be skipped by

readers not interested in technical details.

For a generic running variable \(x_i\) and outcome variable \(y_i\), the smoothness class used by

rdhonest amounts to the following specification, assuming

for simplicity that the cutoff point is \(0\):

\[ y_i = \tau \cdot I(x_i>0) + \beta_1 + \beta_2 x_i + \beta_3 I(x_i>0)\cdot x_i + \text{rem}(x_i) + u_i. \]

The remainder term \(\text{rem}(x)\) has second derivative bounded by \(M\), and satisfies \(\text{rem}(0)=\text{rem}'(0)=0\) (since the function and its first derivative are incorporated into the parameters \(\tau\) and \(\beta\)). Assuming \(u_i\) is mean zero conditional on the \(x_i\)s, the bias of a local linear estimator with estimation weights \(w_i\), conditional on the \(x_i\)’s, is given by

\[ \sum_{i=1}^n w_i \text{rem}(x_i) \]

(this follows by unbiasedness of the local linear estimator under the “correct specification” where \(\text{rem}(x_i)=0\)). A result in Armstrong and Kolesár (2020) shows that, when the weights \(w_i\) are formed from a local linear estimator with a nonnegative kernel, the magnitude of this bias term is maximized when \(\text{rem}(x_i)=-(M/2) x_i^2\cdot \text{sign}(x_i)\):

\[ \text{max. bias} = - (M/2) \sum_{i=1}^n w_i x_i^2\cdot \text{sign}(x_i). \]

We can use this to calculate maximum bias manually, and check that

this matches with the quantity used by rdhonest to compute

a bias-aware CI. The rdhonest command stores the maximum

bias in e(bias).

. * worst-case bias from the previous rdhonest command

. disp e(bias)

.88800705

.

. * calculate worst-case bias manually using estimation weights saved in est_wgt

. gen worst_case_bias_summand = -(e(M)/2)*est_wgt*(margin^2)*sign(margin)

. qui summarize worst_case_bias_summand

. disp r(sum)

.88800705How much wider is the bias-aware CI relative to a CI that uses the

“bias-unaware” critical value 1.96 for a nominal 95% CI? Of course, we

can easily check this for a given data set using rdhonest,

as we’ve already done. To provide a more general answer to this

question, Armstrong and Kolesár (2020)

provide an asymptotic formula that holds when the running variable is

continuous with a positive density. In particular, if the MSE optimal

bandwidth is used and the running variable is continuously distributed

with a positive density, one can approximate the bias-aware 95% CI

computed by rdhonest by replacing the conventional critical

value 1.96 with the number 2.18. Thus, the bias-aware CI is wider by a

factor of approximately \(2.18/1.96\approx

1.11\).

Let’s see how this works with our running example:

. * compute honest CI

. qui rdhonest voteshare margin, kernel("uni")

. disp "[ " e(est) - e(HLCi) " , " e(est) + e(HLCi) " ]"

[ 1.2829887 , 8.3133511 ]

.

. * compute asymptotic approximation using 2.18 rule

. disp "[ " e(est) - 2.18*e(se) " , " e(est) + 2.18*e(se) " ]"

[ 1.3725038 , 8.2238359 ]The approximation is reasonably accurate in this case, leading to a

slightly smaller CI, but not by much. The accuracy of this approximation

might be expected given that the running variable is fairly well-behaved

in this dataset. However, given that rdhonest computes

worst-case bias exactly in finite-samples, there is no need to use

asymptotic approximations to compute worst-case bias.

We’ll illustrate the application of the rdhonest command

to fuzzy RD using the data from Battistin et al.

(2009).

. clear all

. macro drop _all

. webuse set "https://raw.githubusercontent.com/tbarmstr/RDHonest-vStata/master/data"

(prefix now "https://raw.githubusercontent.com/tbarmstr/RDHonest-vStata/master/data")

. webuse rcp

(Battistin, E., Brugiavini, A., Rettore, E., & Weber, G. (2009))

. gen log_cn = log(cn)The outcome variable log_cn is consumption in logs, the

treatment retired is an indicator for retirement and the

running variable elig_year is the number of years since

being eligible to retire. The cutoff is 0.

For fuzzy RD, the syntax is

rdhonest depvar (treat = runvar). As with the sharp RD

example, we’ll begin by using the uniform kernel.

. rdhonest log_cn (retired=elig_year), kernel("uni")

Using Armstrong and Kolesar (2020) rule of thumb for smoothness constant M

Honest inference: FUZZY Regression Discontinuity

──────────────────────────────────────────────────────────────────────────────

Estimate Maximum Bias Std. Error [ 95% Conf. intervals ]

──────────────────────────────────────────────────────────────────────────────

-.154754788 .094148696 .09951997 -.412793464 .103283889

──────────────────────────────────────────────────────────────────────────────

95% One-sided Conf. intervals: (-.412599268, Inf), (-Inf, .103089693)

First-stage estimate: .323809965

Bandwidth (optimized): 5

Number of effective observations: 5018

Parameters:

Cutoff: 0

Kernel: uniform

Optimization criterion: MSE

Standard error estimation method: NN

Maximum leverage for estimated parameter: .000763565

Smoothness constant M (first-stage, rule of thumb): .008178929

Smoothness constant M (reduced-form, rule of thumb): .002849524

──────────────────────────────────────────────────────────────────────────────

Dependent variable: log_cn

Running variable: elig_year

Treatment variable: retired The estimate is the ratio of local linear estimators for the discontinuity at the cutoff in a reduced form and first stage regression. With the uniform kernel, this is numerically equivalent to running an instrumental variables regression controlling for a linear trend on either side of the cutoff, with an indicator for eligibility as the instrument:

. scalar bw = e(bandwidth)

. gen eligible = (elig_year>0)

. gen eligiblexelig_year = eligible*elig_year

. ivreg log_cn (retired=eligible) elig_year eligiblexelig_year if abs(elig_year<=bw), robust

Instrumental variables (2SLS) regression Number of obs = 19,245

F(3, 19241) = 229.84

Prob > F = 0.0000

R-squared = 0.0525

Root MSE = .4489

───────────────────┬────────────────────────────────────────────────────────────────

│ Robust

log_cn │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

───────────────────┼────────────────────────────────────────────────────────────────

retired │ -.3194117 .044604 -7.16 0.000 -.4068394 -.231984

elig_year │ .0123859 .0005108 24.25 0.000 .0113847 .0133871

eligiblexelig_year │ -.0136842 .0069804 -1.96 0.050 -.0273664 -1.94e-06

_cons │ 9.912645 .0099964 991.62 0.000 9.893051 9.932239

───────────────────┴────────────────────────────────────────────────────────────────

Instrumented: retired

Instruments: elig_year eligiblexelig_year eligible

────────────────────────────────────────────────────────────────────────────────────As with the sharp RD example, the point estimate is the same, but the

confidence interval differs since the rdhonest command uses

a bias-aware critical value that takes into account possible

approximation error. Here, we have two reduced form IV equations with

possible specification error, one for the outcome variable \(\log (\text{cn}_i)\) and a first-stage

equation for the treatment variable \(\text{retired}_i\):

\[\begin{align*} \log (\text{cn}_i) = &\tau_{\text{outcome}} \cdot \text{eligible}_i + \beta_1 + \beta_2 \text{elig\_year}_i + \beta_3 \text{eligible}_i\cdot \text{elig\_year}_i \\ & + \text{rem}_{\text{outcome}}(\text{elig\_year}_i) + u_i \\ \text{retired}_i = &\tau_{\text{first-stage}} \cdot \text{eligible}_i + \gamma_1 + \gamma_2 \text{elig\_year}_i + \gamma_3 \text{eligible}_i\cdot \text{elig\_year}_i \\ &+ \text{rem}_{\text{first-stage}}(\text{elig\_year}_i) + v_i \end{align*}\]

The fuzzy RD parameter is

\[ \tau_{\text{FRD}} = \frac{\tau_{\text{outcome}}}{\tau_{\text{first-stage}}} \]

The rdhonest command takes into account the largest

possible asymptotic bias of the estimate over a smoothness class for the

reduced form outcome equation as well as the first stage equation. The

smoothness class is the same one used for sharp RD: we assume that the

remainder term \(\text{rem}()\) comes

from a first-order Taylor approximation at the cutoff (in this case

\(0\)), where the second derivative is

bounded by a smoothness constant \(M\).

The smoothness constant \(M_{\text{outcome}}\) for the reduced form

outcome equation is allowed to differ from the smoothness constant \(M_{\text{first-stage}}\) for the

first-stage equation. These can be specified through the option

m(M_outcome M_firststage). If no options are specified,

then rdhonest applies the rule-of-thumb from Armstrong and

Kolesár (2020) to each of the equations (reduced form outcome

equation and first-stage equation) separately to specify \(M_{\text{outcome}}\) and \(M_{\text{first-stage}}\).

As with sharp RD, the rdhonest command optimizes the

bandwidth for a given criterion specified by

opt_criterion() if no bandwith is specified, with MSE as

the default optimality criterion. For the same reasons described above

for sharp RD, we recommend varying \(M_{\text{outcome}}\) and \(M_{\text{first-stage}}\) and letting

rdhonest optimize the bandwidth, rather than setting the

bandwidth directly (unless the optimized value leads to a very small

number of effective observations such that normal approximation may not

work well). Note that while, in principle, one could further improve

efficiency by using different bandwidths for the first-stage and reduced

form outcome equations, this option is not currently supported by the

rdhonest package.

Let’s try some other values of \(M_{\text{outcome}}\) and \(M_{\text{first-stage}}\). We’ll start with

the rule-of-thumb values used by default in the specification above, and

multiply them by \(1/2\) and \(2\). We can extract these using

e(M) for the outcome and e(M_fs) for the first

stage.

. qui rdhonest log_cn (retired=elig_year), kernel("uni")

. scalar M_outcome_rot = e(M)

. scalar M_firststage_rot = e(M_fs)

.

. scalar M_outcome_05 = .5*M_outcome_rot

. scalar M_firststage_05 = .5*M_firststage_rot

. scalar M_outcome_2 = 2*M_outcome_rot

. scalar M_firststage_2 = 2*M_firststage_rot

.

. qui rdhonest log_cn (retired=elig_year), kernel("uni") m(`=M_outcome_rot' `=M_firststage_rot')

. scalar est_rot = e(est)

. scalar HLCi_rot = e(HLCi)

. scalar h_rot = e(bandwidth)

.

. qui rdhonest log_cn (retired=elig_year), kernel("uni") m(`=M_outcome_05' `=M_firststage_05')

. scalar est05 = e(est)

. scalar HLCi05 = e(HLCi)

. scalar h05 = e(bandwidth)

.

. qui rdhonest log_cn (retired=elig_year), kernel("uni") m(`=M_outcome_2' `=M_firststage_2')

. scalar est2 = e(est)

. scalar HLCi2 = e(HLCi)

. scalar h2 = e(bandwidth)

.

. disp _newline "M_outcome | M_firststage | bw | est. | lower CI | upper CI " _newline ///

> round(M_outcome_05,.0001) " | " round(M_firststage_05,.0001) " | " round(h05,.0001) " | " round(est05,.0001) " | " round(est05-HLCi05,

> .0001) " | " round(est05+HLCi05,.0001) _newline ///

> round(M_outcome_rot,.0001) " | " round(M_firststage_rot,.0001) " | " round(h_rot,.0001) " | " round(est_rot,.0001) " | " round(est_rot

> -HLCi_rot,.0001) " | " round(est_rot+HLCi_rot,.0001) _newline ///

> round(M_outcome_2,.0001) " | " round(M_firststage_2,.0001) " | " round(h2,.0001) " | " round(est2,.0001) " | " round(est2-HLCi2,.0001

> ) " | " round(est2+HLCi2,.0001)

M_outcome | M_firststage | bw | est. | lower CI | upper CI

.0014 | .0041 | 7 | -.0772 | -.2716 | .1172

.0028 | .0082 | 5 | -.1548 | -.4128 | .1033

.0057 | .0164 | 4 | -.244 | -.609 | .121For fuzzy RD, the point estimate is given by \(\hat\tau_{\text{FRD}} =

\frac{\hat\tau_{\text{outcome}}}{\hat\tau_{\text{first-stage}}}\)

where \(\hat\tau_{\text{outcome}}\) and

\(\hat\tau_{\text{first-stage}}\) are

local linear estimates of the discontinuity \(\tau_{\text{outcome}}\) in the reduced form

outcome equation and the discontinuity \(\tau_{\text{first-stage}}\) in the first

stage respectively. The rdhonest command uses the delta

method approximation

\[ \hat\tau_{\text{FRD}} - \tau_{\text{FRD}} \approx \hat\tau_{\text{outcome}} - \tau_{\text{outcome}} - \tau_{\text{FRD}} (\hat\tau_{\text{FRD}} - \tau_{\text{FRD}}) \]

The bias and variance are then computed in the same way as sharp RD. For example, the maximum bias is computed as

\[ \text{max. bias}_{\text{outcome}} + |\tau_{\text{FRD}}| \cdot \text{max. bias}_{\text{first-stage}} \]

where \(\text{max.

bias}_{\text{outcome}}\) and \(\text{max. bias}_{\text{first-stage}}\) are

the maximum bias for each of the reduced form equations, computed in the

same way as for sharp RD. Since \(\tau_{\text{FRD}}\) is unknown,

rdhonest uses an initial value specified by the option

t0() to calculate bias and variance for bandwidth

optimization for the estimate (the default is \(0\)). Then, the point estimate \(\hat\tau_{\text{FRD}}\) is used in the

above formula to compute maximum bias when constructing the CI. Thus,

the CI is asymptotically valid regardless of the initial value specified

by t0(), but the bandwidth is optimal only if a consistent

estimate of \(\tau_{\text{FRD}}\) is

plugged into t0(). See Armstrong and Kolesár (2020)

for details.

Note that the default option t0(0) leads to an

asymptotically efficient bandwidth choice only when \(\tau_{\text{FRD}}=0\). One can obtain an

asymptotically efficient estimate by rerunning the command with

t0(`=e(est)'):

. qui rdhonest log_cn (retired=elig_year), kernel("uni")

.

. rdhonest log_cn (retired=elig_year), kernel("uni") t0(`=e(est)')

Using Armstrong and Kolesar (2020) rule of thumb for smoothness constant M

Honest inference: FUZZY Regression Discontinuity

──────────────────────────────────────────────────────────────────────────────

Estimate Maximum Bias Std. Error [ 95% Conf. intervals ]

──────────────────────────────────────────────────────────────────────────────

-.243983953 .078178872 .126823328 -.533125871 .045157965

──────────────────────────────────────────────────────────────────────────────

95% One-sided Conf. intervals: (-.530768636, Inf), (-Inf, .04280073)

First-stage estimate: .309048375

Bandwidth (optimized): 4

Number of effective observations: 3677

Parameters:

Cutoff: 0

Kernel: uniform

Optimization criterion: MSE

Standard error estimation method: NN

Maximum leverage for estimated parameter: .000989375

Smoothness constant M (first-stage, rule of thumb): .008178929

Smoothness constant M (reduced-form, rule of thumb): .002849524

──────────────────────────────────────────────────────────────────────────────

Dependent variable: log_cn

Running variable: elig_year

Treatment variable: retired While this may lead to a some improvement in CI length, this may come

at the expense of finite sample performance, due to the extra

uncertainty introduced by using the initial estimate to compute the

bias-variance tradeoff. This is similar to the tradeoff between

asymptotic optimality and finite sample performance with feasible

generalized least squares or two-step generalized method of moments. For

this reason, the default implementation simply uses \(0\) for the t0() option.

The delta method approximation described above relies on asymptotics.

This is not an issue for discrete running variables per se, since the

formulas for \(\text{max.

bias}_{\text{outcome}}\) and \(\text{max. bias}_{\text{first-stage}}\)

that the rdhonest command plugs into this delta method

approximation are valid in finite samples, including a discrete running

variable. However, the delta method approximation will break down if the

estimate of \(\tau_{\text{FRD}}\) is

inconsistent, which will be relevant when the number of support points

of the running variable is small, or in “doughnut designs,” where

observations with the running variable near the cutoff are discarded.

Furthermore, this approximation will not work under “weak instrument”

asymptotics where \(\tau_{first-stage}\) is zero or small

relative to the sample size.

To compute honest CIs with better finite sample performance in

settings where such concerns are relevant, one can apply an

Anderson-Rubin approach with honest CIs for sharp RD, as proposed by

Noack and

Rothe (2019). In particular, to test the null hypothesis \(H_0:\tau_{\text{FRD}}=\tau_{\text{null}}\)

using this method, one forms the outcome \(\text{outcome}_i - \tau_{\text{null}} \cdot

\text{treat}_i\) and runs rdhonest with \(M\) set to \(M_{\text{outcome}}+|\tau_{\text{null}}|\cdot

M_{first-stage}\) using the m() option. One can then

do this for a grid of values of \(\tau_{\text{null}}\) to form a CI, taking

care to set \(M\) to \(M_{\text{outcome}}+|\tau_{\text{null}}|\cdot

M_{first-stage}\) for each value of \(\tau_{\text{null}}\) in the grid. The CI is

formed by collecting the values of \(\tau_{\text{null}}\) in the grid for which

the test fails to reject. Noack and Rothe (2019) provide

an R package that does this automatically. To implement this

functionality in the RDHonest package, one can code this grid and loop

manually (please cite Noack and Rothe (2019) in

addition to Armstrong

and Kolesár (2018) if you are computing such an interval).

This section discusses some options that are not directly supported

by RDHonest-vStata. Some of these options are implemented

in the R package or packages written by other authors, or can be

implemented in the RDHonest package using some additional coding.

Clustered standard errors are now included in the R package. While

not yet available in the Stata package, one can run the

rdhonest command to compute the worst-case bias. One can

then run an equivalent regression using the regress command

(restricting to a discontinuity sample or using weights corresponding to

the bandwidth used by rdhonest) to get the same point

estimate along with an option for clustering to obtain a cluster robust

standard error. Note that this will give different results from the R

package if the optimal bandwidth is used, since the R package uses a

variance estimate that allows for dependence when computing the optimal

bandwidth.

One may wish to include additional regressors, which can be interpreted as making a smoothness assumption on a partialled out outcome regressions, as discussed in Appendix B.1 of Armstrong and Kolesár (2018). Support for additional regressors is in progress.

The smoothness class used by RDHonest-vStata assumes

that the second derivative of the conditional expectation function on

either side of the cutoff is bounded by \(M\). This is a Hölder smoothness

class of order 2. Alternatively, once can use impose only an upper bound

on the magnitude of the Taylor approximation, which leads to the

Taylor or Sacks-Ylvisaker smoothness class. If the

Taylor approximation comes from a second derivative bound, then this

will be conservative, which is why the rdhonest Stata

command uses the Hölder smoothness class. However, the

Taylor/Sacks-Ylvisaker smoothness class is available in the R version of

the package.

An alternative smoothness class based on an assumption that maximum

error from a global polynomial approximation is taken away from the

discontinuity point is used in Section IV.B of Kolesár and Rothe (2018). This class is not

implemented in the RDHonest Stata package, but is available in the

RDHonest R package. Note that the second derivative bound used by

rdhonest corresponds to the smoothness class used in

Section IV.A of Kolesár and

Rothe (2018).

One may also want to consider higher or lower order smoothness (bounding a different derivative), or shape constraints. Kwon and Kwon (2020) consider the case of an monotonicity and bounds on the first derivative.

Formulas for minimax affine estimators using arbitrary convex smoothness classes based on convex programming are given in Donoho (1994) and Armstrong and Kolesár (2018). They can be implemented on a case-by-case basis using convex programming.

The rdhonest command does not support different

bandwidths on either side of the cutoff. This is motivated in part by

calculations in Section D.1 of the supplemental appendix of Armstrong and

Kolesár (2020), which show that there is little further

efficiency gain from using different bandwidths on either side of the

cutoff unless there is a very large jump in the conditional variance at

the cutoff.

For fuzzy RD, the rdhonest command uses the same

bandwidth for the first stage and reduced form outcome regressions. If

the smoothness relative to conditional variance is substantially

different in these regressions, one may wish to use different

bandwidths. While this is not supported directly, one can run the first

stage and reduced form outcome regressions as sharp RD specifications to

obtain the maximum bias for each regression, which can then be plugged

into the asymptotic formula given above. However, the variance formula

will depend on the covariance of these estimates, and will need to be

coded manually.

Efficiency results in Armstrong and Kolesár (2020)

show that the default triangular kernel used by rdhonest is

97.28% efficient among all possible weights in typical asymptotic

settings. Nonetheless, one may gain some efficiency by numerically

optimizing the weights, particularly with small samples and irregular

design points.

Fully optimal weights were implemented by Armstrong and Kolesár (2018) for the Taylor class and are available in the R version of this package. For the Hölder class considered here, they are implemented by Imbens and Wager (2019) and available in the accompanying software package.

Armstrong and

Kolesár (2018) derive efficiency bounds showing that the form of

CI used by rdhonest (fixed length bias-aware CIs with

optimized length) are near-optimal among all CIs. These finite-sample

bounds depend on the design points, and can be computed on a

case-by-case basis (although absolute bounds are also given). For the

Taylor class, these efficiency bounds can be computed using the R

version of this package. Asymptotic evaluations of these bounds with a

continuous running variable do not depend on the distribution of the

data; see Armstrong

and Kolesár (2018) and Armstrong and Kolesár

(2020).

As discussed above, rdhonest can be used to compute a

bias-aware version of an Anderson-Rubin style CI in fuzzy RD as proposed

by Noack and

Rothe (2019), although this requires manually looping over a grid

of null values. The R package provided by Noack and Rothe (2019) does

this automatically.